AI: A needed Holiday Interregnum

...time to catch our breath ahead of an AI stuffed 2024

I’ve always this loved this period between Christmas and New Year’s, this Interrgenum between the year past and the year to come. This break to catch our breath between two big holidays. A pause between the frenetic pace of anticipation and stress-inducing anxieties ahead of on set of the Christmas Holidays, and the echoing waves of the same ahead of New Year’s.

And we need in this ‘Year of AI’ more than ever.

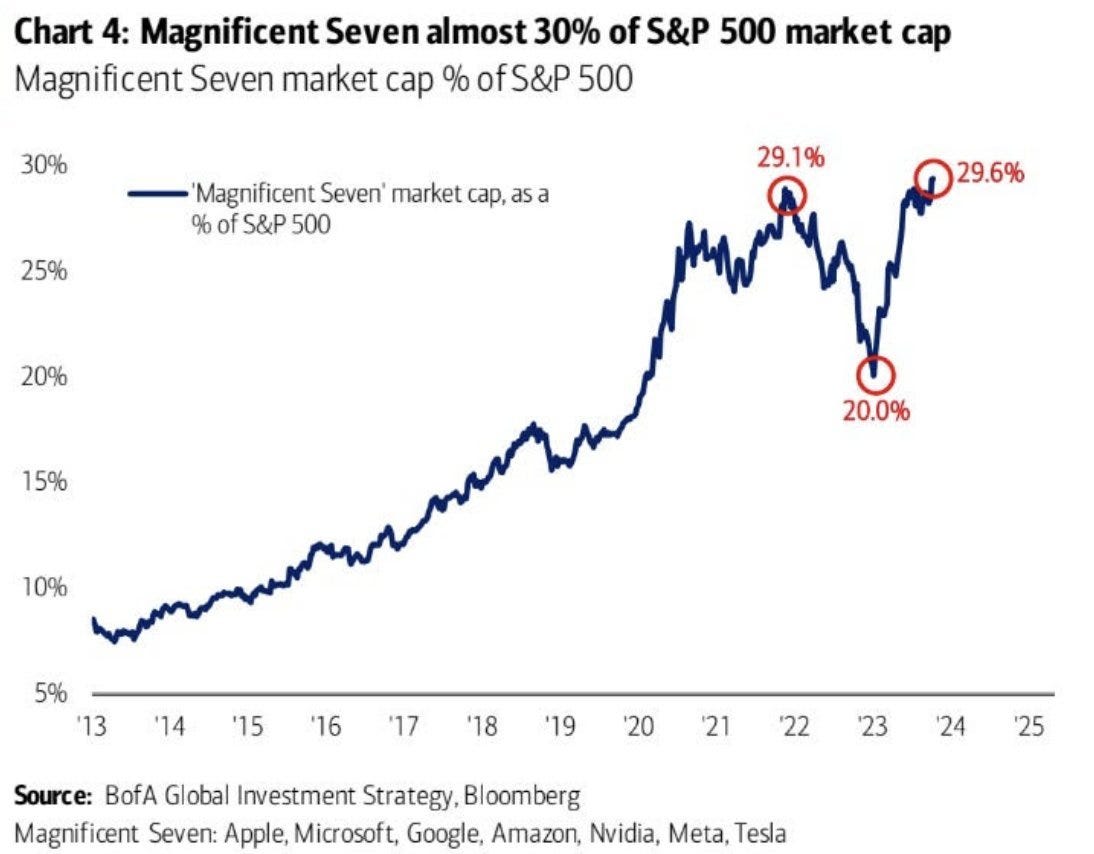

The AI Tech Wave participants of all stripes, are also catching their breath these few days between these two book ends of stress and joy inducing holidays. So it’s a good time to take stock of where we are and where we’re going when the gun goes off for 2024 in the first days of the New Year. Especially for the ‘Magnificent 7’ big tech companies have have helped drive the stock market benchmarks to near-record levels on AI tailwinds.

All the companies large and small are set to hit the ground running at that time. OpenAI, with Microsoft’s assistance, after it’s dramatic end to the first year of ChatGPT’s shot hurt around the world, is poised to close potentially concurrent secondary and primary round of capital raises that may take their valuation to a $100 billion or more.

Microsoft and CEO Satya Nadella is now more keenly than ever focused on driving their now more investor critical than ever AI partnership with OpenAI forward commercially, while navigating OpenAI board and governance expanding exercise in early 2024.

Their rival Anthropic is also finishing up big round of late-year fund raising with two Magnificent 7 big techs Google and Amazon. while racing with OpenAI to put additional Safety safeguards on their otherwise ‘Full-Speed ahead’ plans for next-gen LLM AIs. Both are doing their best to reassure the public and regulators that they have this AI ‘Speed vs Safety’ balancing thing front and center on their operating dashboard.

Google is set to ramp up their now announced three-pronged Gemini LLM launch plans at the start of the year. I continue to call Google’s AI shot in 2024 to augment Search with AI despite some market concerns.

Apple is ramping up to launch their Vision Pro platform a month ahead of schedule in February instead of March. And likely doing a lot more things on AI small and large in the inimitable Apple way.

Nvidia is racing to make sure they can ramp up millions of AI GPU chips and data center infrastructure for both AI training and inference ahead of rivals like Intel, AMD, Qualcomm and so many others next year. TSMC of course is laser focused on making the chips in its fabs for all of the above. And Elon of course is rabidly focused on optimizing all his options AI Grok and others, using his AI morphing global megaphone X/Twitter.

Meta led by that other ‘Magnificent 7’ founder/CEO Mark Zuckerberg, is threading the needle well between open and closed source Foundation LLM AI models led by its Llama 2 and Pytorch AI software infrastructure strategy. As I will expand on in future posts, the whole closed vs open AI debate is likely to increasingly be a distinction without a difference. Open source AI efforts will very much be an important driver for innovation worldwide, but every company commercializing AI, large or small, open or closed, will be focused on commercial opportunities around its AI products and services.

Investors private and public are still seeing AI as something that helps their portfolios going into the New Year despite the hundreds of billions being deployed far ahead of AI ‘product-market-fit’ and the resultant revenues and profits in the years to follow.

And researchers, scientists and engineers in the millions worldwide are frenetically trying to move the exponential opportunities and challenges around hallucinating AIs large and small, to broader utility at scale for both businesses and consumers. While of course improving their understanding of these technologies actually do the things they’re starting to do.

Speaking of businesses, they’re trying to figure out how to engineer LLM AIs into their internal and external work flows at scale, investing billions, while reassuring investors and customers that they got this AI thing handled. Despite early signs that it’s likely going to take longer than currently thought to make it all work at scale. And that their customers will not balk at the higher prices being asked for AI augmentation. Not to mention of course the countless publishers and content creators on the internet whose content is the data fodder and ‘reinforcement loops’ for the multimodal LLM AIs in the first place. Good times for lawyers.

Regulators worldwide are also making sure they’ve got their ducks lines up in terms of the right sequence of ‘Ready, Aim, Fire’ in 2024, especially when over half the world is going through critical elections in so many countries large and small. And politicians of course ‘threading the needle’ with China.

And all AI stakeholders of course trying to figure out how to deal with regular folks who’re trying to make sense of this AI thing in the first place. These mainstream folks, who are being inundated with the possible existential fears around AI, while also hearing breathless tales of how AI ‘will change everything’. And of course the real possibilities for AI driven ‘mischief’ in elections small and large to come. All parties on either side of course trying to leverage the inevitable human urge to anthropomorphize the AI now and to come.

So…we all can use this Interregnum between the Holidays, this ‘Year of AI’ more than ever before. This pause to catch our breath between the software driven reign of deterministic computing of the past with the probabilistic computing of the future at hand.

It’s a timely moment indeed to catch our breath this week. And get ready for New Year’s and beyond. Stay tuned.

(NOTE: The discussions here are for information purposes only, and not meant as investment advice at any time. Thanks for joining us here)