AI: Year-end 2023 for ‘Magnificent Seven’

...quarterly earnings and a whole lot of AI

It’s that time of year again, quarterly earnings season. Know it feels like only yesterday we saw the Big Tech companies report their quarterly results, with tail-winds of investor enthusiasm for the AI Tech Wave. As we roll into the end of the year, these companies now known as ‘The Magnificent 7’, (previously known as FAANGs), are again poised to generally report results in-line with analysts’ positive expectations, buoyed again by AI enthusiasm going into earnings season. As explained here by Blackrock:

“Seven mega cap US-based companies – Apple, Microsoft, Amazon, Google, Nvidia, Tesla, and Meta (Facebook) – have stayed top of mind for many investors this year. These companies have been dubbed the “Magnificent Seven” (not to be confused with the 1960s movie or 2016 remake), are the largest U.S. based companies by market cap, and have performed very well so far in 2023 partially due to the latest artificial intelligence boom.”

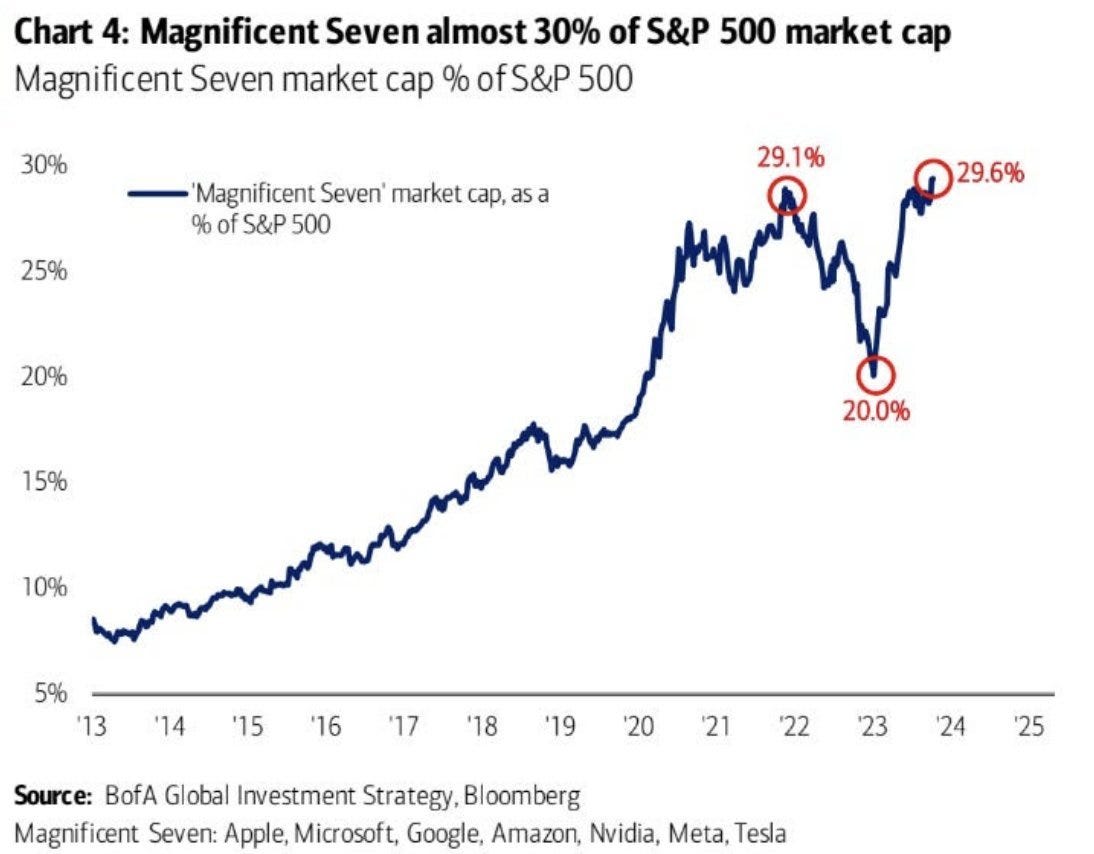

Their returns have been strong over years past and into this year for the seven, to now comprise almost 30% of the S&P 500’s market cap. This can be seen in the multi-year chart below (via Maverick Equity Research). Note the volatility just in the last few months.

As Reuters outlined earlier today:

“High noon is approaching for the market's biggest stocks, as pressure grows on richly valued technology and growth companies to deliver robust earnings at a time when sky-high bond yields threaten to dull the allure of equities.

“Huge rallies for the so-called "Magnificent Seven" stocks – Apple (AAPL.O), Microsoft (MSFT.O), Alphabet (GOOGL.O), Amazon (AMZN.O), Nvidia (NVDA.O), Tesla (TSLA.O) and Meta Platforms (META.O) – have driven nearly all of the S&P 500’s 12% year-to-gain because of their outsized weighting in the index.”

“That stellar performance has also raised the stakes in the upcoming earnings season. Valuations have swelled, with the Magnificent Seven trading at an average forward price-to-earnings ratio of 33.5, compared with the S&P 500's P/E of 18.3.

At the same time, Treasury yields at 16-year highs are providing investment competition to stocks. With U.S. government bonds now offering risk-free yields of around 5% or more, investors may be less forgiving of companies which are unable to deliver strong results.”

Tesla reported their results yesterday, slightly below expectations, with the stock down about 5%, and the others are to report in the few weeks ahead. Again, as Reuters summarizes it:

“That appeared to be the case for Tesla, the first of the megacaps to report results this period. Shares of Tesla were down 7% on Thursday morning after the electric vehicle maker missed Wall Street estimates on third-quarter gross margin, profit and revenue.”

“Everybody knows these guys are going to make money," said Sameer Samana, senior global market strategist at the Wells Fargo Investment Institute (WFII), referring to the Magnificent Seven. "The only question is how fast is that earnings growth, and have investors overpaid for it."

But expectations are still in the positive column for the group, as Investor’s Business Daily sees it:

“Magnificent Seven may be gearing up for a fantastic finish for 2023”.

“All of these companies, with the possible exception of Apple, are seen in some part as artificial intelligence plays, with Nvidia and Microsoft among the big leaders. Nvidia stock, Meta Platforms and Tesla, which have more than doubled in 2023, while Amazon stock and Google have run up more than 50%. Microsoft and Apple stock, the laggards of the megacap group, are up more than one-third this year.”

They have a stock by stock tally and discussion for those looking for a deeper dive.

Fast Company provides broader context of the performance of these seven companies beyond the S&P 500 index performance cited above:

“Through September, the Seven accounted for 75.7% of the Wilshire 5000 Total Market Index’s return for the year, according to numbers that Wilshire sent me. That’s more than triple the Seven’s combined 23.8% weight in the index as of the end of September. (I’m using the Wilshire—which had 3,410 stocks and $42.6 trillion of market value when last I looked—to show you how important the Select Seven have been in terms of the total market’s results.)”

“The difference between the Seven’s weight in the index and their share of the Wilshire’s results means that the Seven have produced total returns (price gains plus reinvested dividends) that dwarf the collective returns of the other 3,400 or so stocks in the Wilshire.”

“Having a mere handful of stocks wield such enormous influence is very unusual. “I haven’t seen this big a concentration at the top since I joined S&P in 1977,” says Howard Silverblatt, senior index analyst at S&P Dow Jones Indices.”

“As a result of the Seven’s terrific performance from the start of the year through August 31, their combined Wilshire weight rose to 24.2% from 18.6%.”

“Their influence would be even greater if we were benchmarking them against the Standard & Poor’s 500 Index, which had 503 stocks and $37.8 trillion of market value at the end of September.”

“As you can see from the month-by-month numbers (see chart), in February and May the Seven accounted for more than 100% of the Wilshire’s total return. That’s astounding—that means that the index would have lost value but not for this small handful of stock over-performers. And in March, they accounted for almost the entire return.”

All of above is of course is on the financial side of the current AI cycle in the AI Tech Wave. The valuations are moving to the optimistic side of the spectrum despite AI product demand and pricing visibility. And the secular side of course also is proceeding strongly with every one of the so called ‘Magnificent 7’ having their AI initiatives and plans underway. Have written extensively about all of them on those fronts.

With less than two and a half months left in 2023, and some of those weeks taken up by holidays, there’s a lot crammed in the next couple of months by Big Tech companies and Regulators on the AI front.

November 6 sees OpenAI’s Developer conference, where Microsoft will continue to be a strong key partner. On the financial side, OpenAI is proceeding with their secondary private tender share offering at a $80 billion valuation, nearly triple the earlier level, valuing the company at over 60 times their estimated annualized revenue for 2023. It makes it one of the highest valued firms backed by venture capital.

Google is expected to roll out their next generation Gemini LLM AI as well in the coming weeks. Meta and Amazon are stepping up strong monetization initiatives around their AI driven product and services elements. Nvidia continues to focus on their DGX data center strategy and there will likely be notable developments there before year-end.

Apple of course is continuing to work on their LLM AI strategy on both the cloud and local devices front. And Elon at Tesla, X and xAI is working on AI initiatives, not the least of which is his ‘Dojo’ AI compute initiative that goes up against Google and Nvidia AI infrastructure in particular. All the LLM AI initiatives from everyone are going multimodal this year as well. And the AI tailwinds continue for big tech along with big investments.

So it’s going to be a busy few weeks before the year is out for all the ‘Magnificent 7’., both in terms of quarterly financial and secular AI driven initiatives. And my 2023 and next three year AI outlook pieces remain on track.

It’d be an understatement to say it’s been a frenetic year in AI innovation and building, since OpenAI kicked off the LLM AI gold rush with ChatGPT just ten months ago. We used to say an Internet year in the 1990s was seven years in ‘regular years’. With the AI Tech Wave, that may feel a tad slow. Lot to look forward to and process ahead. Stay tuned.

(NOTE: The discussions here are for information purposes only, and not meant as investment advice at any time. Thanks for joining us here)

M7 quite a bucket ... great coverage, thank you, have a good weekend!