AI: About Tech and public Equities

...big tech AI tales wag the market

As this year comes to a close a year after OpenAI’s ‘ChatGPT moment’ that kicked off the gold rush in the AI Tech Wave last November, it’s clear that for now the big tech ‘Magnificent Seven’, most with market caps over a trillion dollars each, rule the public market roost. Some might say their AI tales are wagging the relative smaller cap ‘dogs’ in the market (pun intended). As the WSJ notes today in “What the Stock Market Taught Us This Year: Don’t Fall for These Investing Traps”:

“A handful of tech and tech-related stocks, weight-loss drugs and artificial-intelligence providers offer the sum total of stock-market outperformance this year. Beyond these headliners, there is less and less attention on individual names.”

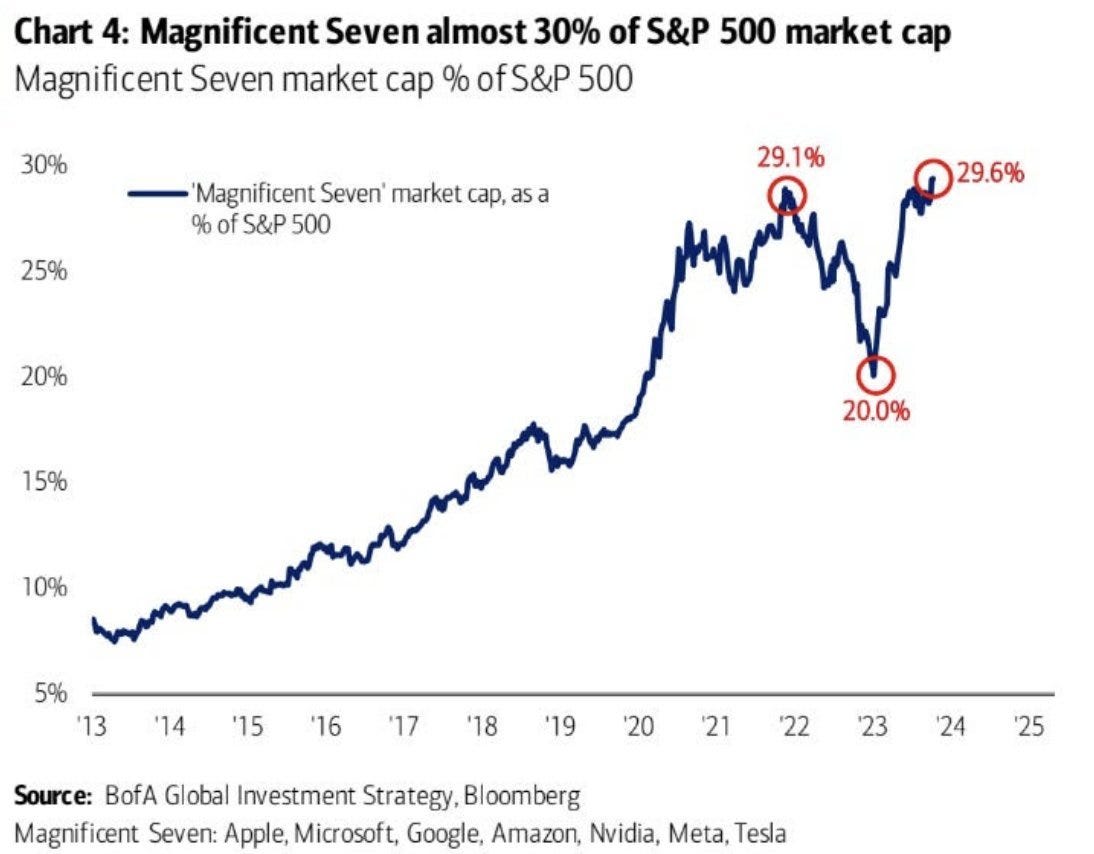

“Those tech behemoths, dubbed the “Magnificent Seven,” account for more than 30% of the index and 87% of its return through October. Let us say that again: Just seven stocks represent one-third of the S&P 500 index. Some now consider Google parent Alphabet, Amazon.com, Apple, Facebook parent Meta Platforms, Microsoft, Nvidia and Tesla to be defensive businesses that can grow through any economic cycle.”

“We’ve seen this before, and the lesson is always the same: Winner-takes-all can dominate over shorter time frames but is rarely a winning bet in the long run.”

This concentrated performance of the AI boosted performance of big tech is something I’ve covered at length in these pages. As this other WSJ piece also today “How Long Can the ‘Magnificent Seven’ Stocks Hold the Line?” notes:

“As in the eponymous 1960s Western, the so-called Magnificent Seven stocks keep on winning. This also means investors are betting the farm on just a handful of bullets hitting their targets.”

“The S&P 500 is in a bull market, fueled by soft inflation data in the U.S. and Europe and the widespread belief that interest rates will start coming down early next year. Yet the stock market has become so top-heavy that speaking of a “bull market” carries less meaning than before.”

Without the key seven stocks listed above and talked about at length on this site, the WSJ adds:

“The high-growth, technology-related companies that analysts have dubbed the Magnificent Seven—the S&P 500 would be up only 8% this year, rather than 19%. Indeed, these stocks inched higher Tuesday even as the broader equity market faltered.”

The issue becomes complicated in a public market increasingly dominated by index investing, which for individual investors in abstract is an eminently wise way to invest in stocks for the long term. But the ‘Magnificent 7’ concentration means that:

“That poses a conundrum for investors, who increasingly use index funds. Right now, buying an S&P 500 tracker means investing 30% of the money in just seven stocks. Historically, the top seven have accounted for 21% of the benchmark, taking the end-of-year average of the past decade.”

Again, something I’ve noted before, illustrated by the chart above.

And this means a stratification in valuations in this concentration:

“This not only runs counter to the principle of diversification, but also means the most important stocks investors own are pricey. The seven stocks have posted strong profits lately, but they are still trading at an average of 32 times forward earnings, compared with 19 times for the broader index.”

Of course, all assets are ultimately driven by the realities and perceptions of where interest rates are and might go, in the much larger bond markets. Investors in both private and public markets are of course adjusting from over a decade of aberration ally low interest rates (aka ZIRP, RIP for now). As the earlier WSJ piece noted:

“The extremely low interest rates that have persisted for much of the past two decades. Over the past 50 years, U.S. interest rates have averaged 5.98%. Today’s 5.5% rate seems high compared with the 0.25% paid during the recession of 2008, but no comparison to 1980 when rates topped out at 20%.”

“Similarly, at the start of the new millennium, a 30-year fixed-rate mortgage was 8.08%—basically in line with 2023 levels, but significantly higher than the bargain 2.96% rate that could be had just two years ago.”

“Higher interest rates now feel like a shock to our systems because we got anchored to some extreme lows. When considered in the full context of a longer history, though, they are in line.”

“Now people are anchored to the S&P 500 beating everything else. But just as we have seen with interest rates in 2023, the trend will revert to the mean, even if it takes a while.”

Of course on the tech and AI front, I’ve long made a point of making sure investors separate financial cycles from secular technology cycles. They’re almost never in sync. This post is to highlight the broader realities of the financial cycles for now. Again, as the WSJ notes in their piece on the ‘Magnificent Seven’:

“With so much market value concentrated in those seven stocks, the benefits of diversifying into small-caps can be severely reduced when a few of their company-specific investments pay off, the research also suggests. The artificial-intelligence boom sparked by OpenAI’s ChatGPT, which has already helped chip-maker Nvidia triple its revenues relative to a year earlier, could be just such a payoff.”

“But reliance on big idiosyncratic effects cuts both ways. Who will benefit most from AI is still an open question. And other megatrends are underpinning the value of the Magnificent Seven, such as Meta’s metaverse or Tesla’s self-driving cars, that are showing less promise.”

“With valuations working against the giants of the stock market, investors are ultimately placing bets on a few massive, unpredictable technological developments. In the film’s end, only three gunmen survive.”

We’ll continue to focus on the secular technology trends for most of our discussions here on the AI Tech Wave. But from time to time, it’s important to continue to take measure of how the tales of the ‘Magnificent Seven’ which for now dominate the multi-billion dollar buildup of AI infrastructure in this gold rush, continue to wag the broader public equity markets. Stay tuned.

(NOTE: The discussions here are for information purposes only, and not meant as investment advice at any time. Thanks for joining us here)