AI: Getting through the Quarter

...'Mr. Market' digests Five 'Magnificent Seven' earnings results

Five done, two more to go of the multi-trillion dollar ‘Magnificent Seven’. The public markets (aka ‘Mr. Market’) seemed to like Microsoft and Amazon’s results a bit better than Google (Alphabet), Meta, and Tesla earlier in the week, judging from the intra-day trading this week. As Bloomberg notes in “Big Tech Sheds $386 billion in value as earnings disappoint”:

“The so-called Magnificent Seven technology companies that have powered this year’s US stock rally are posting disappointing earnings, wiping about $386 billion off their market value and threatening to push the S&P 500 into a correction.”

“Google owner Alphabet Inc., Tesla Inc., Facebook parent Meta Platforms Inc. and Microsoft Corp. have all slumped since reporting, with the latter dragged down in Thursday’s rout.So far, As I said a few days ago in “Year-end 2023 for ‘Magnificent Seven’,”

The above doesn’t include Amazon, which reported after the close today, with for now a positive reception by ‘Mr. Market’.

As I noted just a few days ago:

“It’s that time of year again, quarterly earnings season, for ‘The Magnificent Seven’: Apple, Microsoft, Amazon, Google, Nvidia, Tesla and Meta (aka Facebook)’. All poised again to report results at least in-line with analysts’ positive expectations, buoyed again by the ‘AI Tech Wave’ enthusiasm going into earnings season.”

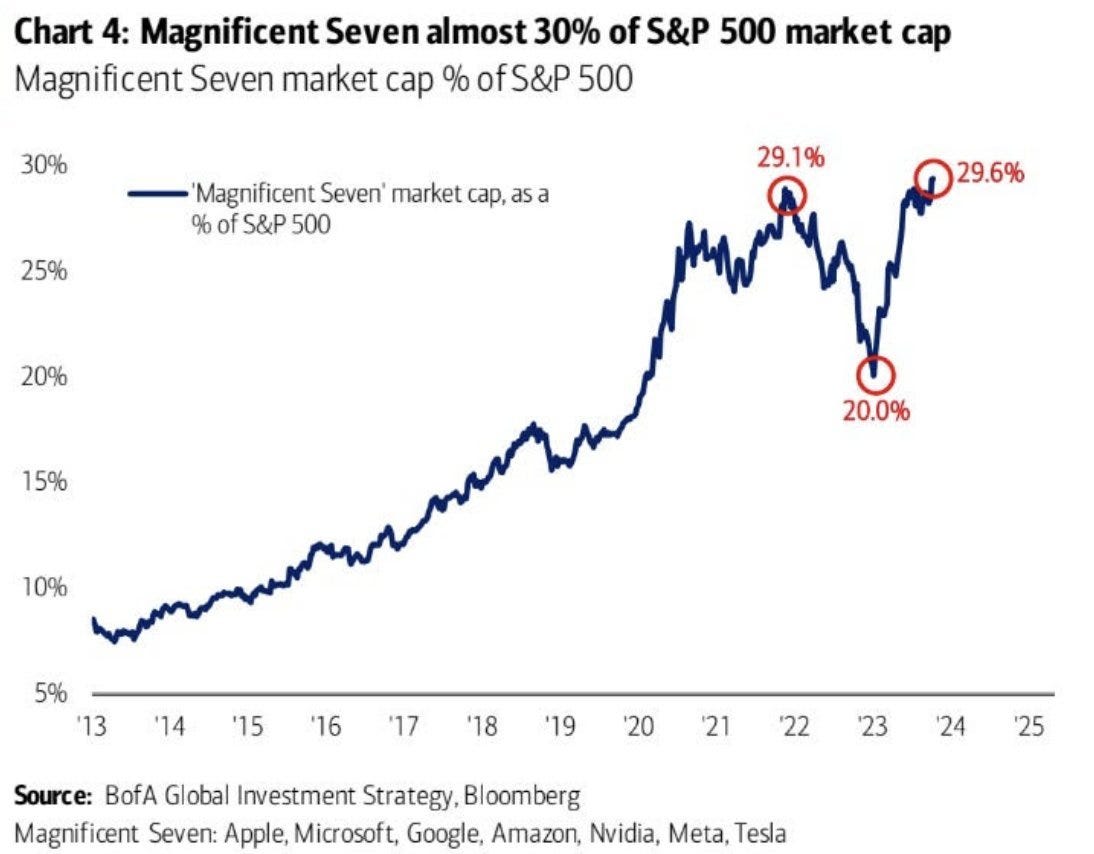

Remember those seven companies are already almost 30% of the S&P 500 over the past few years, with recent momentum related to the AI gold rush optimism in the private and public markets (via Maverick Equity Research). ‘Mr. Market’ likes Big Tech, and this AI stuff, for now.

So as I said earlier, five of those seven reported this week, all mostly with good, in line results, but Mr. Market didn’t like Google’s AI prospects in the near term as it did for Microsoft and Amazon. And had issues with Meta’s results as well, despite otherwise solid results. Remember, all the big tech stocks have done well this year, so some re-tracement for some of them on quarterly results is to be expected. Waves lapping in the ocean.

Microsoft got the most immediate kudos and tailwinds from its AI product and enterprise sales momentum, leveraging its now epic partnership with OpenAI and its GPT-4 and ChatGPT. As the WSJ recounts in “Microsoft Earnings Growth Accelerates in stronger than expected Cloud Demand”:

“Microsoft’s sales growth accelerated last quarter as demand for its cloud computing services heated up amid growing enthusiasm about artificial intelligence.”

“The company reported Tuesday that its revenue grew 13% to $56.5 billion for the quarter through September. That was above analysts’ expectations and a step up from growth of 11% during the year-earlier period.”

“The growth rate in Microsoft’s Azure cloud business was 29%. While that was below the pace that Microsoft posted in the same quarter last year, it was above the preceding quarter and analyst expectations. It gained around 3 percentage points from demand for AI services.”

“Microsoft is one of the first technology titans to report quarterly results. Like many in tech, it has been managing a sharp slowdown and reducing staff and other costs after years of high growth when the pandemic shifted work and life online.”

Microsoft also seemed to benefit from its enterprise sales breadth with business customers relative to its partner OpenAI, as the Information recounts:

“Less than a year after OpenAI launched ChatGPT and built a considerable consumer business, several big companies that were also early customers of its AI, such as Salesforce and Wix, say they are using less expensive alternatives. Some of those firms are paying for similar AI from competing providers that claim they can help the firms use AI more cheaply.”

“Other customers are beginning to buy OpenAI’s software through Microsoft because they can bundle the purchase with other products. That’s a problem for OpenAI, as Microsoft keeps much of the OpenAI-related revenue it generates.”

Scale matters, and Microsoft is reaping the short-term benefits of having the best LLM AI product to sell via one of the broadest enterprise sales forces. Not to mention continued tail winds with products like CoPilot for Github, which now counts over a million paying developers as subscribers.

Google on the other hand, is still ramping up their AI related products and services via Google Cloud, the third cloud data center player after Amazon and Microsoft, and it showed in their quarterly results. Again, as the WSJ framed it in “Google’s Cloud Sales disappoint as advertising rebounds”:

“Google reported its strongest business growth in more than a year but disappointed investors with relatively weak cloud-computing sales, delivering a mixed picture as it continues to wrestle with competitors developing artificial-intelligence tools.”

Again, AI momentum was the focus for investors, despite strong results in other core Google businesses.

Amazon didn’t disappoint the same investors on the AI front, as the Information headlines in “Amazon cranks up its AI Euphoria”:

“Amazon’s artificial intelligence growth is a sight to behold. No, the company didn’t report how much money it’s making from AI, and it probably won’t anytime soon. We’re talking about the expanded use of AI buzzwords in its earnings release. References to Bedrock and CodeWhisperer—two generative AI products from Amazon—rose 67% and 200% in the third-quarter release compared to the second quarter, while mentions of Anthropic—the hot AI startup Amazon recently invested in—quadrupled.”

“We’re teasing! But also not: Amazon is working very, very hard to show how on the ball it is when it comes to the generative AI craze, in part to counter the perception that it has lost a step in AI to its biggest rival in cloud computing, Microsoft. On a call with investors, in fact, Amazon CEO Andy Jassy kept the AI-gasm going as he rattled off the ways Alexa, stores and other Amazon businesses are using the technology. Amazon’s third-quarter results show why. Its AWS cloud unit grew only 12% year over year, the same rate of growth as in the second quarter and down dramatically from 28% in the third quarter of last year. Compare that to the 29% growth Microsoft reported on Tuesday for its Azure cloud unit—which it credited to demand for its AI services—and you can see why Amazon might be a bit concerned. “

All the reports are worth perusing for their non-AI operations and commentary. The five companies are doing fine if one takes a bit of a longer term perspective. Especially Google and Amazon as I’ve discussed already on their AI opportunities.

But I highlight all this to emphasize what’s got ‘Mr. Market’s’ attention for now, given the overall performance of these and other tech stocks’ outperformance this year, in the public and private markets. Irrespective of the post-quarter volatility. The financial market optimism and tail-winds remain on that AI stuff in this AI Tech Wave.

Even though these are early days. Even though the financial momentum will tend to lag the secular momentum of the early LLM AI technologies being trialed and slowly deployed by enterprises. Even though the technology is not yet as safe, reliable, available and affordable as it eventually will be.

Even though businesses are trying to hire ‘AI developers’ in a market where regular coders are rapidly trying to teach themselves AI software and ‘become’ qualified AI programmers. Even though we’re increasingly in a world where geopolitics are making the global tech supply and talent chains more gummed up than all previous tech cycles. Even though regulators everywhere are trying to manage AI for the fears and risks, long before the opportunities are clear, some racing ahead of others.

Even though users are still figuring out what AI is good for and how to even begin to use it. Even though enterprises are figuring out the open vs closed versions of AI products. Even though they’re trying to sort out the ‘narrow’ applications of AI while they await the wider, more general applications that may be safer and more reliable. Even though they’re trying to figure out ‘Big AI’ applications in the cloud from the ‘Small AI’ on local devices.

Even though the vendors and their customers are trying to sort out the right pricing for these new-fangled AI products and services. Even though all that will take multiple quarters measured in years to sort it all out. Even though this always happens in all major technology waves in cycles.

Nope. All that matters less for Mr. Market right now. The FOMO and excitement around AI is propelling the financial cycles ahead of the realities and risk factors of the technology-driven secular cycles, both in the public, and the less transparent private markets, driven currently by corporate strategic imperatives. In a non-zero interest rate environment globally.

It’ll all sort out eventually. In the meantime there’re more big tech reports to come, beyond these five ‘magnificent sevens’ thus far. Apple reports November 2, and Nvidia on November 21st, both after market close.

It’s all ebb and flow, and the financial markets will do their thing vis a vis the secular market realities of this AI Tech Wave. Keeping track of both is the fun and rewarding part.

Just recognize that this quarterly earnings cycle is barely a step forward in the ultra triathlon games ahead. More to come, from ‘Mr. Market’. Stay tuned.

(NOTE: The discussions here are for information purposes only, and not meant as investment advice at any time. Thanks for joining us here).