AI: A New AI driven 2024 ahead

...how we fared vs expectations past six months

The Bigger Picture, December 31, 2023

Six months ago and roughly 180 daily posts on AI ago, I published my AI Outlook for the second half of 2023. I’d stressed that these are still very early days in the AI Tech Wave.

Those six months of 2023 are now of course coming to a close today. In today’s ‘Bigger Picture’, I’m reviewing how the last six months have fared vs my expectations. We’ll review it again mid-year at the end of June of next year. And of course my AI outlook for the next three years. For now, let’s get started on the near-term look at the six months past and ahead.

It doesn’t feel like just six months have passed. So much has happened in AI terms this year, and at such a frenetic pace. There used to be a saying in the Internet boom years of the nineties than an internet year was seven regular years. We need to update that for the AI years. Perhaps half a year in AI terms may end up being seven regular years. Something to think about on another day.

The key expectations for the second half of 2023 as the AI world looked on June 28th this year, were as follows:

“AI still being invented and re-invented”: Although 2023 has seen a lot of AI innovations, like progress in multimodal AI systems from companies like Meta, Google, and of course OpenAI/Microsoft and others, much more needs to be done, especially in the area of AI reliability and reducing hallucinations. I suspect that may take longer than the next six months of 2024. We are still at these systems hallucinating a quarter of the time or more. The other big area of innovation has been in open source ‘Small AI’ systems that run on local devices. Have high hopes here for the year to come, especially from Apple.

“Early days in Horse race”: For most of 2023, it certainly looked like OpenAI and Microsoft had the race all but sewn up. Especially after their partnership and launch of ChatGPT last November. And of course the successes since then. But they had self-inflicted stumbles and dramatic recoveries along the way. And a lot of companies have done pretty impressive things, not the least of it being Google with Bard augmenting Google Search, and Gemini LLM AI systems to come early next years. I’m still calling Google as being the near-term winner in AI Augmented Search this year and beyond. But this and other races continue into 2024.

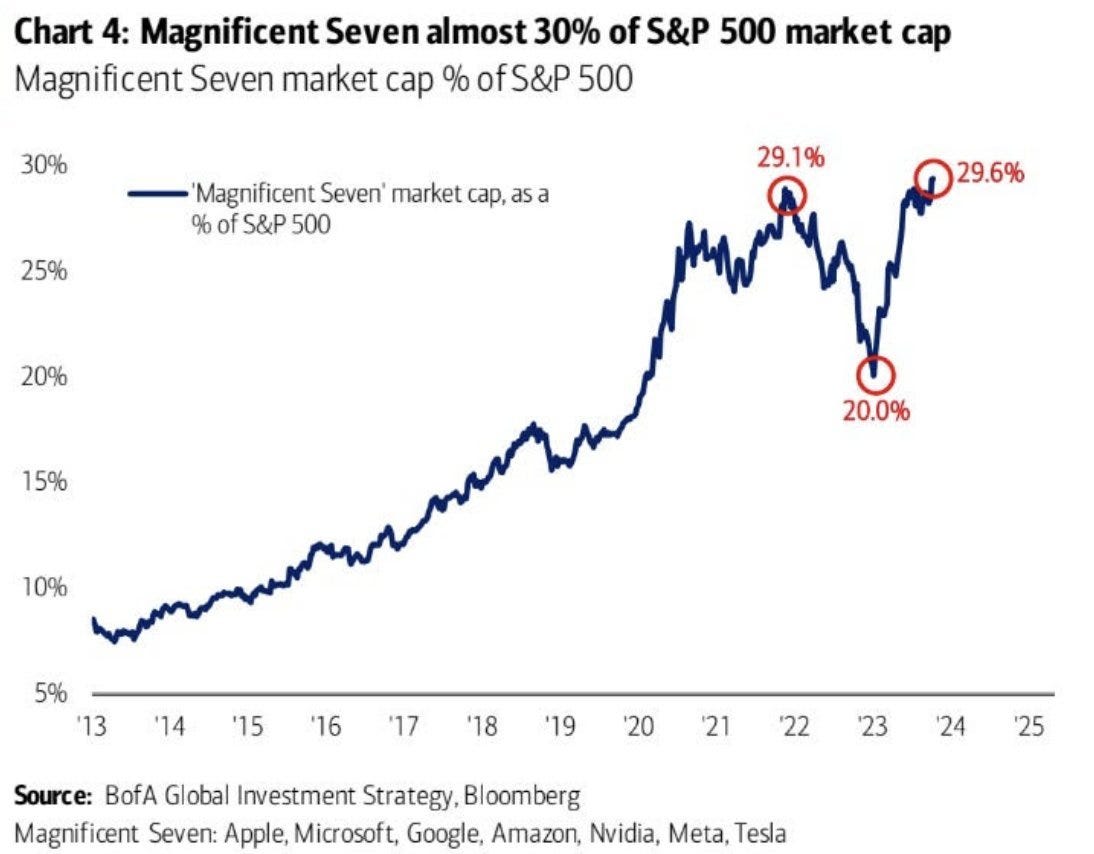

“Chip Constraints Continue”: GPU shortage issues saw Nvidia, up almost 250% in 2023, deliver the best stock market performance among the ‘Magnificent 7’ big tech companies. Collectively their leadership and public market enthusiasm for AI stories drove the Nasdaq up over 50% this year, better than the other market averages which also had near record performances. Chip constraints will likely continue into 2024 and potentially into 2025. But TSMC and other chip fabs have been ramping up enough to mitigate some of those shortages. Lot more to track here in 2024.

“Beware AI Veneers”: As I mentioned in an earlier post, most of the AI multi-hundred billion in investment this year has been in using current AI technologies to augment and add-on existing software and hardware technologies with new AI capabilities. What I’ve called ‘AI veneers’. What I call ‘AI Native’ innovations, especially in multimodal and particularly voice driven AI innovations, are a smaller fraction of the overall progress. But those are the ones that capture most of the headlines. That certainly won’t change in 2024. Watch this race.

“Rising Regulatory Drumbeats”: There was a lot of frenetic activity on this front, especially with Europe and the EU running ahead with their EU AI Act. That will still likely take at least a couple of years or more to be streamlined and put into effect. The US saw the White House issue a voluminous set of AI Executive Orders this year, and the Senate and Congress have planned much more AI related deliberations into 2024. Key here is how restrictive these regulations can get ahead of the actual AI innovations that potentially may be the most risky over time. That AI ‘Speed vs Safety’ issue is the current bane of the AI industry, having already almost stopped OpenAI in its track late this year. Expect lots more drama here in 2024.

“Geopolitics trump globalized tech supply chains”: And of course the US-China efforts to ‘thread the needle’ despite the national security and trade issues around technology and geopolitics continue into 2024. What’s been encouraging is that despite a lot of aggressive actions on both sides driven by politics, both sides have so far kept their eye on the longer term ball of their true north longer-term interests to cooperate rather than compete more contentiously. For now the better ‘Cooperation’ focused Prisoner’s Dilemma Game Theory continues in practice.

As I’ve said in my ‘catch our AI breath’ Interregnum piece on Christmas day, we have a lot more to pay attention to in 2024. not least of it being the massive investments and aggressive moves by all the tech companies big and small.

Tomorrow brings a New Year with an accelerating amount of AI driven change. Enjoy the New Year’s Eve celebrations today, and let’s brace ourselves for 2024. Stay tuned.

(NOTE: The discussions here are for information purposes only, and not meant as investment advice at any time. Thanks for joining us here)