AI: 'Boomerang' Deals

... separating investments & revenues

One of the headline grabbing aspects of the OpenAI and Microsoft partnership, was the $11 billion plus investment by Microsoft, starting with a billion in 2019 and over $10 billion last year.

The partnership has many unique characteristics, not the least of which is the co-existence of a non-profit and profit structure for OpenAI, and capped returns for investors including Microsoft for their 49% stake in the company.

It’s always been clear that billions of those investments would go back to Microsoft’s Azure Cloud business for the massive hardware and software ‘Compute’ infrastructure that OpenAI needed to build and train its current and next generation Foundation LLM AI models from GPT3 to GPT4 and beyond.

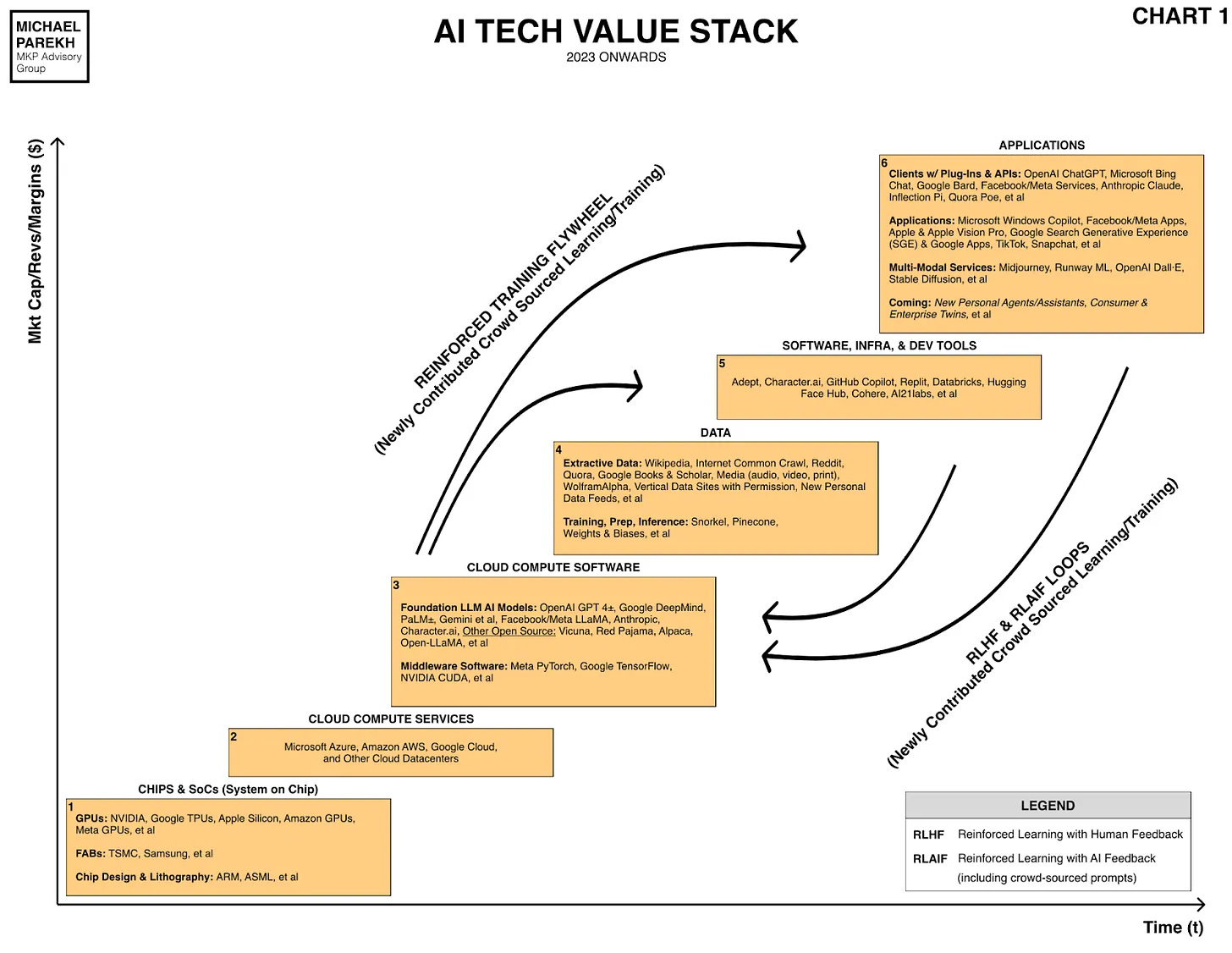

So for Microsoft, this investment also means revenues for one of its core businesses, Azure Cloud, that Wall Street values highly relative to larger competitors like Amazon AWS, and smaller ones like Google Cloud, Oracle Cloud, and many other cloud data center providers. (Boxes 2 and 3 in our AI Tech Value Chart below).

This ‘left pocket to right pocket’, ‘boomerang’ money flow is characteristic of most Tech waves in the early ‘Gold Rush’ building phase, and this wave is no different. Investments turn into revenues for given periods of time.

The dollar amounts are much larger this time around, given the scale of investments needed for LLM AI Infrastructure, and the billions of potential customers globally for AI products and services down the road. Both consumer and enterprise customers potentially, showing up in boxes 5 and 6, in our chart above

This separation of investments and revenues is worth pointing out for a couple of reasons. First, these are relatively big dollars for even Microsoft, as will point out below. Second, we are seeing these deals accelerate to many companies besides OpenAI and Microsoft.

On the first point, a new revelation via some court filings this week was the relative size of Microsoft’s Azure business and Amazon AWS. It was smaller than analysts expected:

“Microsoft has never disclosed Azure Cloud revenues; bundled together with Windows Server, SQL Server, Enterprise Services as part of Intelligent Cloud segment.

Azure = $34bn 2022 revenue

AWS = $72bn 2022 revenue

The revelation that Azure was only half the size of AWS, was a surprise.”

So some part of $8-10 billion of Microsoft’s OpenAI investment coming back as Azure business as revenues, is important to note.

This week saw Inflection AI, a new ‘AI Native’ Startup founded by the ex-founder of Google’s Deepmind AI business, raise another $1.3 billion from investors including Nvidia, the company making the critical GPU chips that make the AI magic happen. And the ones that are in short supply at least into next year globally, despite curbs on sales to China (topic for another day).

As Inflection points out, they’re getting at least 22,000 Nvidia top of the line H100 GPUs to build their models, worth hundreds of millions of dollars. And some of the other investors include data center companies like Coreweave, that Nvidia is also an investor in, providing them with the much in demand GPU chips and related ‘Compute’.

We are seeing the same round-trip, or ‘boomerang’ characteristics in this other deal this week by Runway, the leading AI video company, raising $141 million from investors including Nvidia, Google, Salesforce, and other infrastructure providers.

Again, these investment and business deals are all par for the course in every tech wave. And there are more examples. But the details are important to track, especially for public investors, as they compare the infrastructure companies’ business against each other, and sequentially over time (quarter over quarter growth comparisons going forward).

And for investors and media not to be overly impressed with the headline investment announcements above the fold. Stay tuned.